Life Insurance

Life insurance isn’t just about what happens after you’re gone — it’s about how confidently you live today, knowing your family is protected no matter what.

A Gift of Certainty in an Uncertain World

Our Guardianship of Assets strategies, which is the third step to achieving total financial freedom, include:

- Insurance planning

- Legal protections

- Risk management techniques

We ensure that your loved ones are well-protected, allowing you to focus on growing your wealth without undue worry.

Providing financial security to beneficiaries upon death as well as protecting your assets is crucial to maintaining financial freedom. This step involves safeguarding your accumulated:

Providing financial security to beneficiaries upon death as well as protecting your assets is crucial to maintaining financial freedom. This step involves safeguarding your accumulated:

- Investments

- Real estate properties

- Other valuable assets

from potential risks and estate taxes.

Your life insurance payout always goes to whomever you choose — tax-free.

The money can be used to pay bills, the mortgage, kids’ education, wealth for the next generation, or to keep your business running.

Your life insurance payout always goes to whomever you choose — tax-free.

The money can be used to pay bills, the mortgage, kids’ education, wealth for the next generation, or to keep your business running.

Modern Insurance Programs Tailored to You

Meeting the needs of our clients’ risk management and estate planning objectives often involves the use of insurance products.

Today, more than ever, there is a broad range of modern insurance programs tailor-made for specific protection requirements.

As an independent broker, we are ideally positioned to search the market for:

Today, more than ever, there is a broad range of modern insurance programs tailor-made for specific protection requirements.

As an independent broker, we are ideally positioned to search the market for:

- The best product

- At the best price

- To meet your specific needs

Types of Life Insurance Plans Available

Term Life Insurance

Affordable, temporary peace of mind

- Provides coverage for a specified period (e.g., 10, 20, or 30 years or to age 65/75)

- Death benefit paid only if death occurs during the term

- Lower premium costs than permanent policies

- No cash value

- Best for temporary needs:

- Mortgage protection

- Children’s education

- Family income replacement

Term to 100

Affordable, permanent peace of mind

- Life insurance coverage to age 100

- Considered a permanent plan

- No cash values or dividends → Lower premiums

- Ideal for permanent needs:

- Funeral costs

- Supplementing income

- Estate taxes

- Dependent child care

Permanent Life Insurance

Wealth Creation and Protection with Guaranteed Growth

Includes variations like:

- Whole Life

- Universal Life

- Variable Life

- Provide lifetime protection

- Leverage tax advantages

- Serve estate planning, wealth creation, and insured retirement goals

Life Insurance for Seniors & Hard-to-Insure Canadians

Because Everyone Deserves Dignity, Protection, and Peace of Mind

We specialize in policies for:

- Seniors

- Diabetics

- Individuals with hard-to-insure conditions

✅ No medical exams

✅ Instant quote process

✅ Immediate coverage after purchase

✅ Licensed advisor assistance

Join thousands of satisfied customers who found the right coverage without complications.

✅ Instant quote process

✅ Immediate coverage after purchase

✅ Licensed advisor assistance

Join thousands of satisfied customers who found the right coverage without complications.

Life Insurance Comparison

| Comparison Feature | Whole Life | Universal Life | Term to 100 | Term |

|---|---|---|---|---|

| Period of Coverage | Life | Life | To age 100 | Depends on term contract (e.g., 10, 20 years). Usually not past age 70 or 75. |

| Premium | Guaranteed. Usually level. | Flexible. Can be increased or decreased within limits. | Guaranteed. Usually level. | Guaranteed and level for term. Increases with each new term. |

| Death Benefits | Guaranteed. May increase via dividends. | Flexible. Tied to cash value / funding. | Guaranteed. Remains level. | Guaranteed for the term duration. |

| Cash Values | Guaranteed. Builds over time. | Flexible. Based on investment / deposits. | Usually none. (Maybe small value after 20+ years). | Usually none. (Some may have minimal non-forfeiture value). |

| Non-Forfeiture Options | Guaranteed (based on cash value). | Guaranteed (based on cash value). | Generally none. | Generally none. |

| Dividends | Payable on “participating” policies. Not guaranteed. | Most are non-participating. | Most are non-participating. | Most are non-participating. |

| Advantages | Lifetime protection. Cash value. Potential dividends. | Flexible premiums & death benefit. Tax-advantaged. | Lifetime coverage. Lower initial cost. | Lowest initial cost. Convertible. |

| Disadvantages | Higher initial cost. Less flexible. | Complex. Requires funding. Investment risk. | No cash value. Less flexible. | Premiums rise. Terminates with age. No cash value. |

For more info, visit the Canadian Life and Health Insurance Association (CLHIA).

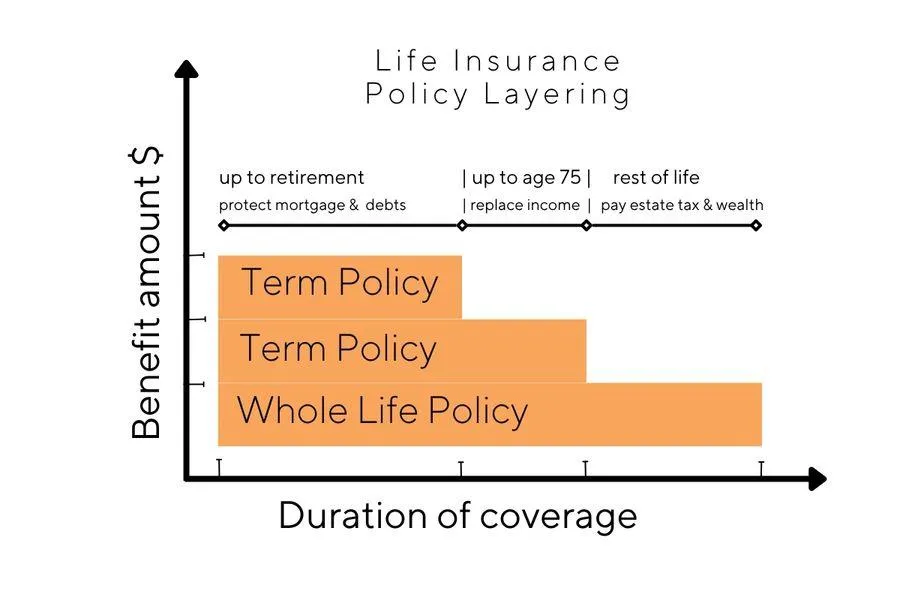

Life Insurance Policy Layering Concept

A well-structured insurance policy provides financial protection throughout all life stages, including:

- ✅ Covering Mortgage Payments

- ✅ Providing Income Replacement

- ✅ Paying Estate Taxes

- ✅ Establishing Personal Legacies

- ✅ Covering Unexpected Medical Expenses

Navigating Your Options: The Hexavision Mentorship Advantage

Understanding:

- • Term Life vs. Permanent

- • Coverage need analysis

- • Tax implications

- • Advanced strategies like Corporate Insured Plans

…can feel overwhelming.

That’s where we come in.

Hexavision believes in empowering Canadians to make smart financial decisions.

That’s where we come in.

Hexavision believes in empowering Canadians to make smart financial decisions.

🎓 Our Free Mentorship Program Includes:

- • Education without bias

- • Personalized policy analysis

- • Guidance through application

- • Empowerment through financial literacy

Partner with us.

Choose the path that serves your goals and your loved ones.

Choose the path that serves your goals and your loved ones.

👉 Book A Call

Take the first step toward peace of mind and lasting legacy.