Disability Insurance Protect your most valuable asset.

Your ability to make income.

Paycheque Protection | A Gift of Certainty in an Uncertain World

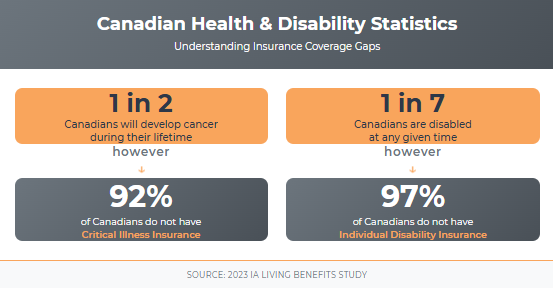

Imagine waking up tomorrow unable to work due to an unexpected illness or injury. Your ability to earn an income might pause, but your bills won’t. Mortgage payments, groceries, utilities, childcare – life’s expenses continue. This is where Disability Insurance becomes your financial safety net. It provides you with regular, monthly payments to help cover your living expenses while you focus on what matters most – your recovery. Shockingly, nearly 40% of working Canadians experience a disability lasting 90 days or longer before age 65. Disability insurance helps ensure that a health challenge doesn’t turn into a financial crisis.

- Keep earning even if illness stops you from working.

- Get monthly payouts to cover essential expenses.

- Plans tailored to your job, needs, and goals.

Our Guardianship of Assets strategies, which is the third step to achieving total financial freedom framework extends beyond traditional wealth management to proactively protect your financial well-being against life’s most challenging moments. This means protecting your ability to make income from serious injury and sickness into your financial plan today, recognizing that preparing for possibilities is vital for lifetime financial security. A disability can significantly threaten your financial stability and long-term goals, potentially depleting hard-earned assets meant for your future and family.

As your independent advisors, we meticulously search the market, leveraging access to modern, often specialized insurance programs. We find the tailored Disability Insurance policy that fits your unique needs, acting as that essential layer of protection. Our personalized guidance demystifies complex options, empowering you with the confidence to pursue your ambitions, knowing you’re better prepared for unexpected health-related financial shocks.

Who Benefits Most from Disability Insurance?

While everyone’s situation is unique, Disability Insurance is particularly crucial if you are:

- Self-Employed or a Small Business Owner: You don’t have an employer’s group plan to fall back on. Your income directly depends on your ability to work.

- The Primary Income Earner: Your family relies heavily on your paycheque to maintain their lifestyle.

- Have Limited Group Coverage (or None): Employer plans might offer basic coverage, but it’s often not enough, especially for higher earners, or may not cover certain types of disability (like mental health) adequately. Individual DI can supplement or replace group plans.

- Want Long-Term Financial Security: You value knowing your income is protected right up until retirement (many plans offer benefits to age 65).

- Don’t Have Significant Emergency Savings: DI prevents you from having to deplete your savings or RRSPs during a health crisis.

- Work in Any Occupation: Disabilities aren’t limited to physical injuries. Mental health challenges, cancer, heart conditions, and chronic pain are common reasons for claims across all professions.

If you rely on your earned income to live, Disability Insurance deserves serious consideration.

Why Choose Disability Insurance? Key Benefits

Income Stability

Receive regular monthly payments (often 60-85% of your pre-disability income).

Peace of Mind

Reduce financial stress during a difficult time, allowing you to focus on recovery.

Protect Your Savings

Avoid draining your retirement funds or emergency savings.

Cover Living Expenses

Ensure you can still pay your mortgage, utilities, and other essential bills.

Tax-Free Benefits

If you pay the premiums personally, the monthly benefits you receive are typically tax-free.

Flexibility

Tailor individual plans with specific waiting periods, benefit durations, and optional riders (like cost-of-living adjustments).

Important Considerations: Policies have specific definitions of disability, waiting periods before benefits begin (e.g., 30, 90, 120 days), and defined benefit periods (how long payments last, e.g., 2 years, 5 years, or to age 65). Understanding these details is key – something your Hexavision mentor can clarify.

Navigating Your Options: The Hexavision Mentorship Advantage

Choosing the right Disability Insurance can feel complex. Terms like “waiting periods,” “benefit periods,” “own occupation,” “riders,” and understanding how individual plans differ from group or government benefits (like CPP Disability or the Canada Disability Benefit) can be overwhelming.

That’s where Hexavision stands apart. We offer no-cost, personalized mentorship to help you understand your options clearly. We’re not just selling a policy; we’re providing guidance. We’ll help you assess your needs, compare features, and understand the fine print before you make a decision, ensuring the coverage you choose truly fits your life and budget.

Learn more about our holistic approach on our Insurance Planning page.

Understanding Disability Insurance in Canada: An FAQ

Disability insurance provides a living benefit and financial protection by replacing a portion of your income if you become unable to work due to illness or injury. It’s important because it helps you maintain your lifestyle and meet financial obligations when you can’t earn an income. If you become disabled and cannot work, you file a claim. If approved, the insurance company will pay you a regular benefit amount, usually a percentage of your pre-disability income, after a waiting period.

Anyone who relies on their earned income to cover mortgage payments and living expenses can benefit from disability insurance. This includes employees, self-employed individuals, and business owners. It protects your ability to earn income even if you are seriously ill or injured.

There are various types, including short-term and long-term disability insurance. Short-term coverage typically provides benefits for a limited period, while long-term coverage can provide benefits for years, potentially until retirement.

The cost of disability insurance is influenced by factors such as your age, health, occupation, the amount of coverage you need, the length of the waiting period, and the benefit period.

Yes, policies can have different definitions of disability. Some policies may require you to be unable to perform the duties of your own occupation, while others may require you to be unable to perform any occupation for which you are reasonably suited by education, training, or experience.

When choosing a policy, consider the benefit amount, the waiting period, the benefit period, the definition of disability, and any riders or options that may be available. It’s also important to understand the policy’s terms and conditions, exclusions, and limitations.

Premiums vary based on your age, health, occupation (risk level), the monthly benefit amount you choose, the waiting period (longer wait = lower premium), and the benefit period (longer coverage = higher premium). It typically ranges from 1-9% of your salary, but a personalized quote is necessary.

STD typically covers the initial period of a disability (e.g., up to 6 months), often provided by employers or EI Sickness Benefits. LTD begins after STD or EI benefits end and covers longer durations, sometimes up to age 65. Individual DI policies usually focus on long-term protection.

Maybe. Group plans are a great start but often have limitations: benefits might be taxed, coverage amounts might be capped (especially for higher earners), the definition of disability might be restrictive (“any occupation” vs. “own occupation”), and coverage ends if you leave the job. Individual DI can supplement group coverage and is portable.

This is crucial and varies by policy. Some define it as being unable to perform the duties of your own specific occupation, while others use a stricter definition of being unable to perform any occupation you’re reasonably suited for by education, training, or experience. Mental health conditions and chronic illnesses are often covered, not just physical injuries. Always review the policy definition.

The goal is typically to replace 60-85% of your pre-disability after-tax income. Insurers have maximum limits based on your earnings. A financial advisor can help calculate the right amount for your needs and budget.