Critical Illness Insurance

Securing Your Finances Against Health Shocks

Shield your finances from the impact of critical illness.

No sales pitch — just honest, expert advice.

Understand what coverage you need and why.

Book on your schedule — no stress, no pressure.

A Gift of Certainty in an Uncertain World

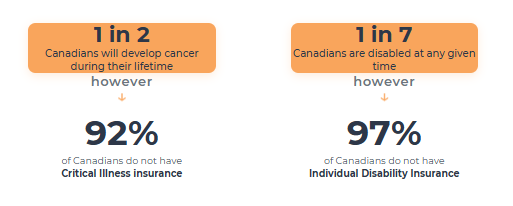

Our Guardianship of Assets strategies, which is the third step to achieving total financial freedom framework extends beyond traditional wealth management to proactively protect your financial well-being against life’s most challenging moments. This means integrating serious illness risk management into your plan today, recognizing that preparing for possibilities is vital for lifetime financial security. A critical illness diagnosis can significantly threaten your financial stability and long-term goals, potentially depleting hard-earned assets meant for your future and family.

That’s why we consider living benefits such as Critical Illness Insurance, a fundamental component of a robust financial strategy. It acts as a crucial safeguard, providing a vital, tax-free lump-sum payment upon diagnosis of a covered condition. This ensures you have the necessary funds to focus on recovery without draining your savings or disrupting your income stream.

As your independent advisors, we meticulously search the market, leveraging access to modern, often specialized insurance programs. We find the tailored Critical Illness policy that fits your unique needs, acting as that essential layer of protection. Our personalized guidance demystifies complex options, empowering you with the confidence to pursue your ambitions, knowing you’re better prepared for unexpected health-related financial shocks.

Who Benefits Most from Critical Illness Insurance?

While anyone can benefit from this protection, it’s particularly valuable for:

- Individuals without significant emergency savings: Provides immediate funds when needed.

- Families with dependents: Helps maintain financial stability and cover household expenses if a primary income earner falls seriously ill.

- Business owners and self-employed individuals: Looking to protect the business should they be unable to work and covers income gaps and business expenses during recovery.

- Those with high-deductible health plans: Helps cover out-of-pocket medical costs.

- Anyone seeking peace of mind: Knowing you have a financial cushion in case of serious illness brings invaluable security.

- Corporations with high-value Executive: business executives or owners with significant retained earnings jointly own critical illness coverage with their company where they share the costs and also the tax and financial benefits.

Understanding Critical Illness Insurance: A Financial Safety Net During Tough Times

In simple terms, Critical Illness Insurance pays you a one-time, tax-free lump sum payment if you are diagnosed with a specific life-altering illness covered by your policy and survive the waiting period (usually 30 days). Think of it as financial breathing room when you need it most. This money is yours to use however you see fit – there are no restrictions. You could use it for:

- Replace lost income if you or a spouse need time off work while you focus on recovery.

- Covering medical expenses not paid for by government plans (e.g., certain treatments, medications, private nursing).

- Making modifications to your home or vehicle.

- Paying off debts like a mortgage or loans.

- Seeking treatment outside of Canada.

- Simply reducing financial stress so you can concentrate on getting better.

Commonly covered conditions often include cancer, heart attack, and stroke, but policies can cover many other serious illnesses.

It’s crucial to understand the specific conditions covered and their definitions within your chosen policy. Please check below given FAQ for list of covered conditions.

The Hexavision Advantage: Guidance You Can Trust

Choosing the right Critical Illness Insurance policy can feel overwhelming. Definitions vary, coverage options differ, and the fine print matters. That’s where Hexavision stands apart.

We offer no-cost mentorship to help you navigate the complexities of Critical Illness Insurance. Our dedicated advisors take the time to understand your unique situation, your concerns, and your budget. We don’t just sell policies; we provide education and personalized guidance, ensuring you select the coverage that truly fits your life and protects what matters most. We believe informed decisions lead to better outcomes.

Learn more about our holistic approach on our Insurance Planning page.

Critical illness insurance Frequently asked questions

Critical illness insurance is to provide financial protection against the costs and lifestyle changes associated with a serious health diagnosis. It acts as a complementary product to traditional and govt. health insurance, offering a financial buffer to help manage various expenses and potential income loss resulting from a covered serious illness.

The benefit of critical illness insurance is paid out as a tax-free, lump-sum cash payment. This payment is made upon the diagnosis of a covered critical illness, provided that the insured has survived for a specified period after the diagnosis (known as the survival period).

The lump-sum payment is highly flexible and can be used for a wide range of needs. This includes replacing lost income due to inability to work, paying for medical treatments not covered by health insurance, making modifications to a home to accommodate a new condition, or even covering travel expenses for specialized medical treatment. The funds are not restricted to direct medical costs.

A crucial aspect is understanding which specific illnesses are covered by the policy. Critical illness coverage is not universal; it is restricted to a predefined list of critical illnesses explicitly specified within the policy document. Eligibility for a claim depends on the diagnosis being for a condition that is listed as covered. Common ones include specific types of cancer, heart attack, and stroke. Many policies cover 25+ conditions like kidney failure, major organ transplant, paralysis, etc. Coverage varies by insurer and policy. Many critical illness insurance policies include the following Critical illnesses and conditions as covered :

Cancers and Tumours:

1. Benign Brain Tumour

2. Cancer (Life-Threatening)

Cardiovascular:

3. Aortic Surgery

4. Coronary Artery Bypass Surgery

5. Heart Attack

6. Heart Valve Replacement or Repair

7. Stroke (Cerebrovascular accident)

Neurological:

8. Bacterial Meningitis

9. Dementia, including Alzheimer’s disease

10. Motor Neuron Disease

11. Multiple Sclerosis

12. Parkinson’s Disease and Specified Atypical Parkinsonian Disorders

Vital Organs:

13. Kidney Failure

14. Major Organ Failure on Waiting List

15. Major Organ Transplant

Accident and functional loss :

16. Acquired Brain Injury

17. Blindness

18. Coma

19. Deafness

20. Loss of Limbs

21. Loss of Speech

22. Paralysis

23. Severe Burns

Other:

24. Aplastic anemia

25. Occupational HIV Infection

+ Long-Term Care In case of loss of independent existence

Critical Illness Insurance pays a tax-free lump sum upon diagnosis of a covered health condition, regardless of your ability to work. Disability Insurance typically replaces a portion of your income on a monthly basis if you’re unable to work due to injury or illness. They serve different, but complementary, purposes as living benefits.