Imagine trying to build your dream home with only a hammer. You could probably put a few things together, but you wouldn’t get very far. For a solid, lasting structure, you need a complete toolbox—saws, wrenches, drills, and more, each with a specific job.

Your financial life works the same way. Yet, for decades, many Canadians have been handed just one investment account as the only tool by traditional financial institutions: the RRSP. It’s been presented as the one-size-fits-all solution for long-term financial well-being, but is it always the right tool for the job? What if there are better options for you? Just think this way, how will you pay less tax in retirement if your goal is to live the same, or an even better, lifestyle than you do today?

Navigating the “alphabet soup” of investment accounts—from the RRSP to the Non-Registered, and now the new FHSA—can feel overwhelming. This confusion often leads to inaction or choosing a path that isn’t optimized for your unique goals. The mission here is to change that. This guide is designed to provide Empowerment Through Knowledge, cutting through the noise to give you the clarity you need to maximize the efficiency of your money at work or in other words, to help you eliminate any leakage of your hard-earned money that may be happening unknowingly and unnecessarily in your current planning.

We are going to open up the financial toolbox the Canadian government has provided and examine each of the four main tools: the Registered Retirement Savings Plan (RRSP), the Tax-Free Savings Account (TFSA), the First Home Savings Account (FHSA), and the Non-Registered account. By understanding the true purpose, mechanics, and tax implications of each, you can start building a personalized strategy that paves your way toward Total Financial Freedom.

Meet Your Financial Toolkit: The 4 Key Canadian Investment Accounts

Before we do a deep dive, let’s lay out the four primary tools in your wealth-building kit. Understanding the primary role of each is the first step in building a powerful financial strategy. The Canadian government designs each to play a unique role in your financial life. Clarity about where to invest your money is essential for long-term success. Each toll determine how much you will end up paying in taxes. The less you know about tax the more you pay. Click here to read about how to Stop Paying Interest-Free Loans to CRA And Keep More Of What You Earn.

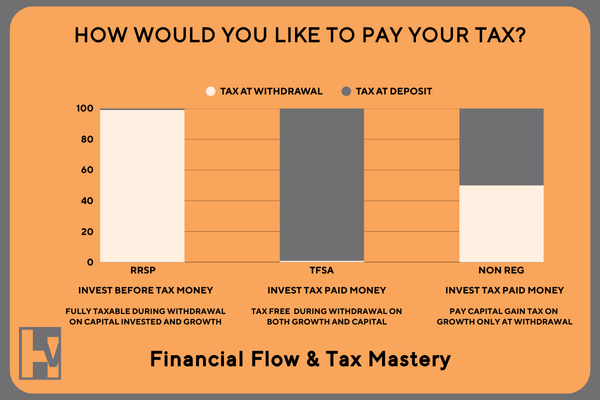

- The RRSP: The Classic Retirement Hammer. Its primary and explicit purpose is to provide you with income in retirement. This is a tool designed to postpone paying your very high taxes until a later date, allowing the pre-tax money to grow over the long term. The goal is to fund your lifestyle after your working years are over, and you are willing to pay tax on both invested capital and all the compounded growth over many years. I like to call this account as “Tax Me Later “

- The TFSA: The Flexible Multi-Tool. This highly flexible vehicle is designed for a wide array of financial goals, not just retirement. Think of it as your go-to tool for everything from long-term highest growth wealth building to an emergency fund to saving for a car, a vacation, or supplementing your retirement income. Never pay tax again on any growth forever, allowing you to withdraw both capital invested along with compounded growth over many years. I like to call this account as “Tax Me Never Again”

- The FHSA: The Specialist’s Power Tool. This account was specifically created to help Canadians save for a down payment on their first home. It’s a highly specialized and powerful tool designed for a single, important life milestone to help you buy your first home. I like to call this account as “Don’t Tax Me for Down Payment”

- The Non-Registered Account: The Overflow Workspace. This is a general-purpose investment account which can be used for investing normally after you have maximized your contributions to your TFSA. It offers complete flexibility as there are no limits on contributions and withdrawals. I like to call this account as “Tax Me As I Go”

Choosing the Right Tool for the Job

| Feature | Registered Retirement Savings Plan (RRSP) | Tax-Free Savings Account (TFSA) | First Home Savings Account (FHSA) | Non-Registered Account |

| Primary Purpose | Retirement savings | Most Flexible savings for any goal, including Wealth Creation | First home purchase savings | General investing after TFSA is maximized |

| Eligibility Age | Any age with earned income; must close at 71 | 18+ (or age of majority) | 18+ (or age of majority) to 71 | Age of majority |

| Contribution Tax Treatment | Tax-deductible at Deposit (before tax funds) | Not tax-deductible (after-tax funds) | Tax-deductible | Not tax-deductible (after-tax funds) |

| Investment Growth Tax Treatment | Tax-deferred | Tax-free | Tax-free | Taxable annually |

| Withdrawal Tax Treatment | Not taxed on withdrawal; gains are taxed when realized | Tax-free | Tax-free (qualifying) or Taxable (non-qualifying) | Not taxed on withdrawal; gains taxed when realized |

| Annual Limit (2025) | Lesser of 18% of 2024 earned income or $32,490 | $7,000 | $8,000 | None |

| Lifetime Limit | None | None | $40,000 | None |

| Contribution Room Carry-Forward | Yes, indefinitely until age 71 | Yes, indefinitely | Yes, up to $8,000 per year | N/A |

| Impact of Withdrawal on Room | Permanently lost | Restored the following year | Varies: Qualifying (none); Non-qualifying (generates re-participation room) | N/A |

| Impact on OAS/GIS | Withdrawals are income; can trigger clawbacks | No impact | Qualifying (no impact); Non-qualifying (can trigger clawbacks) | Realized income can trigger clawbacks |

The Classic Retirement Hammer: The RRSP (Registered Retirement Savings Plan)

For decades, the RRSP has been the veteran of the Canadian investment world. It is, without a doubt, the tool most frequently recommended by traditional financial institutions. The advice is simple: contribute now, get a tax refund, and worry about the rest later.

But at Hexavision, we guide our clients to Rethink Retirement. The entire premise of the RRSP hinges on one critical assumption: that you will be in a lower tax bracket in retirement than you are during your peak earning years. But what if your goal is to live a retirement that is just as comfortable, or even more so, than your life today? A great lifestyle requires significant income, and every dollar of that income from an RRSP is taxable. This is where the conventional wisdom deserves a closer look.

Primary Purpose: Built for your golden years. The RRSP is a savings plan, registered with the government, with the primary and explicit purpose of providing you with income in retirement. Its structure is built to incentivize long-term saving, allowing your nest egg to grow in a tax-sheltered environment until you need to access it.

Who It’s For To open and contribute to an RRSP, you must be a Canadian resident for tax purposes and have “earned income” reported on a tax return. While there’s no minimum age to open one, you can only contribute until December 31 of the year you turn 71. After that, the plan must be converted into a retirement income vehicle, like a Registered Retirement Income Fund (RRIF), or cashed out.

The Core Mechanic: Save Tax Now The RRSP’s main appeal is its powerful, immediate tax benefit. There are two parts to this:

- Tax-Deductible Contributions: The amount you contribute can be deducted from your gross income for the year, which reduces your overall tax bill and often results in a tax refund.

- Tax-Deferred Growth: All investment earnings—including interest, dividends, and capital gains—grow and compound within the plan without you having to pay any tax on them annually.

The Trade-Off: Pay Tax Later This is the critical part of the equation that is often downplayed. You are deferring the tax, not eliminating it. Every single dollar you withdraw from an RRSP is considered income and is fully taxable at your marginal rate in the year you take it out.

If your retirement income needs are high to support the lifestyle you desire, these mandatory, taxable withdrawals could push you right back into a high tax bracket. This can undermine the entire “save-tax-now” strategy and create an unexpected tax burden just when you want to be enjoying your freedom.

The Versatile Multi-Tool: The TFSA (Tax-Free Savings Account)

If the RRSP is the classic hammer, the TFSA is the modern, indispensable multi-tool that every Canadian should have in their kit. Introduced in 2009, it offers a level of flexibility and tax efficiency that fundamentally changes the game of wealth building. For many Canadians, especially those not yet in their peak earning years, the TFSA is often a far more powerful and strategic choice in maximizing the efficiency of their money at work.

Primary Purpose: Ultimate flexibility for any financial goal Unlike an RRSP, the TFSA is not limited to retirement. It is a highly flexible registered tax-advantaged savings and investment vehicle designed for a wide array of financial objectives. It’s an excellent tool for lifelong goals like wealth building or even short- to medium-term goals like saving for a car or a vacation, and its liquidity makes it the ideal location for an emergency fund. It is also a powerful tool for long-term goals, serving as an outstanding supplemental account for retirement savings.

Who It’s For Eligibility for the TFSA is straightforward. You must be a Canadian resident, have a valid Social Insurance Number (SIN), and be at least 18 years of age. A key distinction from the RRSP is that “earned income” is not a requirement to contribute to a TFSA. Your contribution room accumulates automatically every year from the time you turn 18, as long as you are a resident of Canada.

Its Superpower: 100% Tax-Free Growth & Withdrawals This is what makes the TFSA a financial superstar and a cornerstone of Maximizing the Efficiency of Money. While contributions are made with after-tax dollars (meaning you don’t get an upfront tax deduction), that is the last time the tax man ever gets to touch that money. All investment income—including interest, dividends, and capital gains—accumulates and compounds completely tax-free, and all withdrawals are also 100% tax-free. It is your own personal tax haven, fully sanctioned by the government.

The Game-Changing Feature: Contribution Room is Restored This unique feature is what truly sets the TFSA apart. The full amount of any withdrawal you make from your TFSA is added back to your available contribution room on January 1 of the following calendar year. This allows your TFSA to act as a revolving savings pool; you can access funds when needed without permanently sacrificing your ability to shelter money from tax in the future. This makes the TFSA the undisputed champion for your emergency fund. Using an RRSP before a TFSA is highly inefficient for most Canadians, as it triggers tax and permanently destroys your contribution room.

A word of caution: A common and costly error is misunderstanding the timing of this rule. If you withdraw funds from a TFSA, you must wait until the next calendar year to re-contribute that amount without affecting your current year’s contribution limit. Re-contributing in the same year after you’ve already maxed out is considered an over-contribution and will trigger a 1% monthly penalty tax. To learn indepth about TFSA please click here.

The Specialist’s Power Drill: The FHSA (First Home Savings Account)

The newest addition to the Canadian financial toolbox is a true game-changer. Introduced in 2023, the FHSA is like a high-powered drill designed for one job: getting you into your first home faster and more efficiently than ever before. It has fundamentally altered the savings strategy for aspiring homeowners and is a perfect example of an innovative tool that can accelerate your journey.

Primary Purpose: The most powerful tool for saving for a first home The FHSA is a registered plan specifically created to help Canadians save for a down payment on their first home. For any eligible Canadian with this goal, the FHSA is unequivocally the primary and most tax-efficient savings vehicle available. It directly challenges the long-standing primacy of using the RRSP’s Home Buyers’ Plan (HBP) and, for the first $40,000 of savings, is mathematically superior.

Who It’s For To open an FHSA, you must be a Canadian resident, be at least 18 years old (or the age of majority in your province), and be no older than 71. The central requirement is that you must be a “first-time home buyer.” This is defined as someone who has not owned a home in which they lived as their principal residence at any point in the calendar year the account is opened or in the preceding four calendar years.

The “Best of Both Worlds” Hybrid The FHSA’s design is a brilliant hybrid of the most attractive features of the RRSP and the TFSA:

- Like an RRSP, contributions are tax-deductible, reducing your taxable income and providing you with immediate tax relief.

- Like a TFSA, your investment growth and qualifying withdrawals for a home purchase are completely tax-free.

This powerful combination means you get a tax deduction on the way in and pay no tax on your contributions or their growth on the way out—a benefit no other account offers.

A Critical Rule: Your contribution room only starts accumulating after you open an account This is the most important planning point for the FHSA. Unlike the TFSA, where room accumulates automatically from age 18, your annual $8,000 of FHSA contribution room only begins to accumulate after you open your first account. If you are eligible but wait a few years to open one, you permanently forfeit the contribution room from those prior years. This creates a strong incentive for any potentially eligible person to open an FHSA as soon as they qualify, even with a minimal initial deposit, simply to start the clock and begin accumulating their annual room. To learn in-depth about the FHSA account, please click here.

The Unlimited Workspace: The Non-Registered Account

After you’ve maximized contributions to your TFSA—the ultimate tax-efficient, multi-purpose tool in your financial kit—where should your next dollar go? Conventional wisdom often points directly to the RRSP, but for many Canadians, a more strategic and flexible option comes first: the Non-Registered account. Understanding how to use this account properly is key to Maximizing the Efficiency of Your Money. It offers unique advantages that aren’t available in any registered plan.

Primary Purpose: A Hub for Liquidity and Advanced Strategies While this account is often seen as simple “overflow,” its best use is as a strategic hub for your money after your TFSA is full. Because it has no contribution limits, it can be an excellent secondary location for your liquid emergency fund, allowing you to keep your highest-growth potential investments sheltered from tax inside your TFSA.

The “Tax-As-You-Go” Feature Unlike the tax-free nature of a TFSA or the tax-deferred structure of an RRSP, a non-registered account operates on a “tax-as-you-go” basis. You pay tax on investment income in the year it is earned or realized. This means interest is taxed annually, but the tax on capital gains is only triggered when you decide to sell the investment. This gives you a significant degree of control over your annual tax bill that you don’t have with future RRSP withdrawals.

The Upside: A Powerful Tool for Leveraged Investing Here is an advanced strategy that sets the non-registered account apart: it is the ideal vehicle for leveraged investing. Because it is a taxable account, the interest paid on money you borrow to invest can be tax-deductible against your income. This can significantly lower the cost of borrowing and amplify your potential returns. This tax-deductibility of interest is a powerful feature that is not available when investing within a registered account like a TFSA or RRSP. It is a strategic tool that, when used correctly, can dramatically accelerate wealth creation.

By prioritizing the TFSA first and then using a Non-Registered account for liquidity and strategic leverage, you build a powerful and flexible financial foundation before turning to the more restrictive, long-term nature of an RRSP. To learn in-depth about Non-Registered Investment accounts, please click here.

Advanced Strategies for the Savvy Hexavisionary

Understanding the basics of each account is the first step. True financial freedom comes from understanding how these tools work together and how they impact other areas of your financial life. Here are some advanced strategies that move beyond conventional wisdom.

The Retirement Blind Spot: How RRSP Withdrawals Can Affect Your OAS and GIS Benefits

Many Canadians look forward to receiving Old Age Security (OAS) benefits in retirement. However, this benefit is income-tested and subject to a “recovery tax,” commonly known as the OAS clawback. For 2024, this clawback begins once an individual’s net income exceeds $90,997. This is a critical blind spot for those who have saved exclusively in RRSPs. Every dollar withdrawn from an RRSP or a subsequent RRIF is fully included in your net income calculation. Consequently, your own retirement savings can directly trigger or increase the OAS clawback, forcing you to give back a portion of your government benefits. That is why having your investments in both RRSP and TFSA helps in managing taxes during the decumulation phase.

The TFSA’s Hidden Power in Retirement

The TFSA is the strategic solution to the OAS clawback problem. Withdrawals from a TFSA are not considered income for tax purposes. As a result, they have zero impact on your eligibility for OAS or the Guaranteed Income Supplement (GIS). This makes the TFSA an exceptionally powerful tool for retirees. A savvy Hexavisionary can draw the mandatory minimum from their RRIF and then supplement their spending needs with tax-free TFSA withdrawals. This allows you to keep your official net income below the clawback threshold for as long as possible, maximizing your after-tax retirement income.

Is Your Money Safe? A Note on Creditor Protection

This is a vital and often-overlooked risk, particularly for business owners, independent contractors, or professionals. The legal protection of your assets in the event of bankruptcy varies dramatically between accounts.

- RRSP/RRIF: Assets held in these accounts are generally protected from creditors under federal bankruptcy law. (The main exception is for contributions made in the 12 months before bankruptcy).

- TFSA & FHSA: These accounts do not have the same statutory creditor protection. Funds held in a TFSA or FHSA are generally seizable by creditors.

For some individuals, the asset protection offered by an RRSP may be a compelling reason to prioritize its funding, even if a TFSA seems more advantageous from a purely tax-based perspective.

Building a Legacy with Smart Estate Planning

Upon death, the default treatment for an RRSP is for its full market value to be taxed as income on the deceased’s final tax return, which can result in a substantial tax liability. The TFSA, however, offers a uniquely powerful estate planning tool for spouses: the “successor holder” designation. If you name your spouse or common-law partner as a successor holder, they seamlessly take over ownership of your TFSA upon your death. The account maintains its tax-free status and does not impact the surviving spouse’s own TFSA contribution room. It is a simple and elegant way to transfer wealth, preserving a much larger pool of tax-exempt capital for your loved one.

Your Hexavisionary Framework: A Simple Prioritization Strategy

Knowledge is the first step, but action is what builds wealth. The optimal strategy is not one-size-fits-all; it’s a dynamic approach that adapts to your income, goals, and stage of life. Here is a simple framework to help you prioritize.

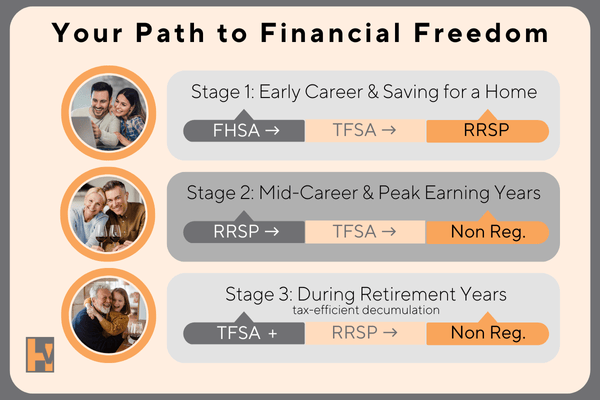

Stage 1: Early Career & Saving for a Home (Priority: FHSA → TFSA → RRSP)

If you are in the early stages of your career with a lower income and your primary goal is homeownership, your focus should be on maximizing tax efficiency for that goal while building a flexible savings base.

- First Priority: FHSA. Contribute up to the $8,000 annual maximum to get the powerful combination of a tax deduction and a future tax-free withdrawal. Opening an account as soon as you are eligible is critical to start accumulating contribution room.

- Second Priority: TFSA. After funding your FHSA for the year, direct your remaining savings to a TFSA. This will build your liquid, tax-free emergency fund and provide flexible savings for other goals.

- Third Priority: RRSP. Contributions are generally less advantageous at lower income levels because the tax deduction is not as valuable.

Learn more about Financial Planning For Millennials In 2025 here.

Stage 2: Mid-Career & Peak Earning Years (Priority: RRSP → TFSA → Non-Registered)

During your peak earning years when you are in the highest tax bracket, your income is higher and the focus shifts toward maximizing tax deductions and accelerating your retirement savings.

- First Priority: RRSP. Make strategic contributions to your RRSP to lower your taxable income, ideally to the bottom of a lower tax bracket. A powerful strategy is to then take the resulting tax refund and contribute it directly to your TFSA, effectively using the government’s tax deferral to fund your tax-free savings.

- Second Priority: TFSA. Once your strategic RRSP contribution is made, your next goal should be to maximize your TFSA contributions.

- Third Priority: Non-Registered. For individuals who have maxed out all available registered accounts, the non-registered account is the next logical step for continued, unlimited investing.

Stage 3: Pre-Retirement & Retirement (Priority: TFSA is King)

As you approach and enter retirement, the strategy shifts from accumulation to tax-efficient decumulation, with a heavy emphasis on preserving your wealth and government benefits.

- First Priority: TFSA. In retirement, the TFSA is your most valuable tool. Continue to maximize contributions if possible. It becomes your primary source for drawing tax-free income to supplement your pensions and RRIF withdrawals without triggering OAS clawbacks.

- Second Priority: Spousal RRSP. If there is a significant income gap between you and your spouse, contributing to a spousal RRSP can be a powerful income-splitting tool to reduce your household’s overall tax burden in retirement.

- Third Priority: Non-Registered. Focus on structuring your investments here to be as tax-efficient as possible, prioritizing assets that generate capital gains over those that generate highly taxed interest income.

We began this journey by imagining your finances as a toolbox. As we’ve seen, the RRSP, TFSA, FHSA, and Non-Registered accounts are all powerful tools, but a tool is only as effective as the person wielding it. The key to building lasting wealth is no longer about blindly following the conventional wisdom of using one tool for every job.

True financial success comes from strategically selecting the right tool for the right purpose at the right time in your life. This is the essence of Maximizing the Efficiency of Money. By understanding the unique strengths and strategic applications of each account, you can build a cohesive plan that works in harmony with your goals. To learn more about comprehensive financial planning, please click here.

You now have the foundational knowledge to challenge old assumptions, to Rethink Retirement, and to start architecting a plan that is truly your own. You have taken the first and most important step on the path from uncertainty to Empowerment Through Knowledge. But this is just the beginning. Building a comprehensive plan to achieve Total Financial Freedom requires a framework and mentorship. If you are ready to move beyond the basics and implement advanced strategies tailored to your unique situation, we invite you to learn more about Hexavision’s Financial Mentorship program. Discover the Hexavisionary Framework and join the community of Hexavisionaries who are taking control of their financial destiny. Contact us to start your journey today.

Frequently Asked Questions (FAQ) about Choosing Investment Accounts

Which is better for me, an RRSP or a TFSA?

What is the main advantage of the First Home Savings Account (FHSA)?

Can I contribute to an RRSP, TFSA, and FHSA all in the same year?

What happens if I take money out of my RRSP before retirement?

The entire amount you withdraw is considered income in that year and is fully taxable at your marginal tax rate.

The contribution room that you originally used for that deposit is permanently lost and is not added back in future years.

Is the TFSA a good account for retirement savings?

What is the penalty for over-contributing to my registered accounts?

RRSP: A penalty tax of 1% per month is imposed on excess contributions that exceed your deduction limit by more than a cumulative lifetime buffer of $2,000.